3Q rental growth slows for national logistics & industrial markets - JLL

Contact

Oct 22, 2024

3Q rental growth slows for national logistics & industrial markets - JLL

JLL’s 3Q 2024 Research figures show face rental growth slowed quarter-on-quarter in 3Q, annual growth remains very strong, discussed JLL’s Head of Logistics and Industrial – Australia, Peter Blade and JLL’s Head of Strategic Research – Australia, Annabel McFarlane.

Face rental growth has slowed in Q3 for logistics and industrial real estate markets. Effective rents fell nationally by 1.8% as incentives increased in most markets, recording the first negative quarterly reading since March 2021.

JLL’s 3Q 2024 Research figures show face rental growth slowed to 0.9% quarter-on-quarter in 3Q. Annual growth remains very strong, recording 12.5% year-on-year.

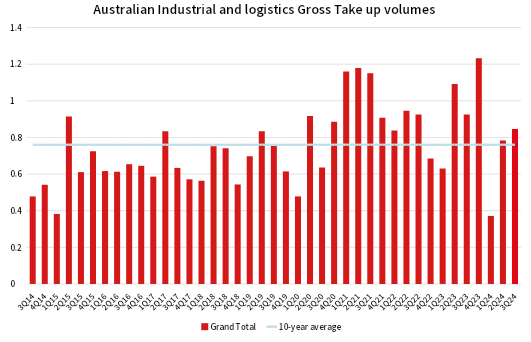

Occupier demand continues to rebound, as gross take up increased again in 3Q to 845,500 sqm and was up on first and second quarter 2024 totals, and the 10-yr quarterly average of 760,310 sqm per quarter. JLL recorded 71 occupier moves in 3Q which is also the highest reading for this year.

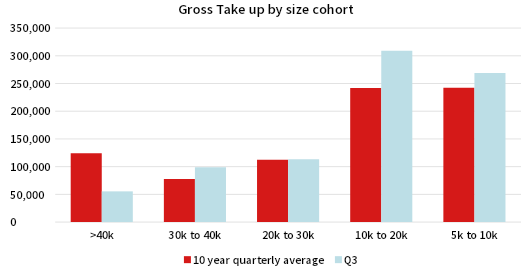

Third party logistics providers (3PL’s) take up increased to 301,000 sqm, accounting for 37% of all activity. However, behind the headline number activity, take up volumes are above average this quarter in all size cohorts, except >40,000 sqm illustrating a notable shift from strategic expansion to real estate activity based on contracts.

Prime and secondary face rental growth was recorded in 15 and 13 out of the 22 tracked precincts for the quarter.

Key markets in Brisbane, Sydney and Melbourne recorded mixed net face rental growth, with solid gains in Sydney’s Inner West (1.1% q-q) and Outer South West (1.7% q-q) and Brisbane Southern (1.6% q-q) and minimal growth in other East Coast markets.

However, effective rents edged lower as developers and landlords compete for tenants, and incentives have increased. Effective rents peaked in late 2023 in most markets and have corrected by 4.0% in Sydney Outer Central West, 4.4% in Brisbane Southern and 6.9% in Melbourne West over the first 9 months of 2024 East Coast markets.

Adelaide was a notable outlier this quarter. Incentives in the Adelaide market range from 0% to 20% depending on precinct and stabilised in 3Q24 following uplifts in some precincts earlier in the year. Low availabilities and limited supply has pushed strong quarterly rental increases in nearly all precinct ranging from 3.8% q-q (North West) and 6.2% (Outer south). A disciplined approach to supply is supporting rental growth in the Adelaide market. Assets under construction and due to complete by the end of 2025 are already 77% pre-committed.

JLL’s Head of Logistics and Industrial – Australia, Peter Blade, said: “The logistics occupier market has changed substantially over the course of this year. 3PL companies are waiting to secure a particular contract before they commit to new facilities. Additionally, many are still rightsizing distribution networks down from elevated levels maintained over the last four years, in line with eCommerce demand normalising.

“Holding costs are likely to impact developers in markets where land values and land tax rates have increased substantially, and land tax bills have more than doubled. We expect this to increase the probability of developers pushing the go button for serviced sites with development approval, moving to construction phase without a precommitment.

“For these developers, success with this strategy will require getting asset size right to meet demand,” said Mr Blade.

JLL’s Head of Strategic Research – Australia, Annabel McFarlane, said: “NAB’s Online retail sales index showed Australia’s online penetration rate has increased again to 13.5% in July 2024 from the trough recorded at 12.9% in 2022. The world of online shopping is still growing as consumers have made it part of their daily lives and this bodes well for the long-term resilience of logistics occupier demand.”

Notable right sizing activity from large transport logistics occupiers has supported robust demand for existing space in 3Q24 which accounts for 64% of all take up volumes. These groups have absorbed some large tranches of sublease space in the Melbourne and Brisbane markets.

Related Readings

South East Melbourne is Australia’s tightest industrial market - JLL | The Industrialist

Mixed results for logistics in 2Q24 - JLL | The Industrialist

Adelaide is running out of room for industries - JLL | The Industrialist

Important Information:

Contact details:

Contact details:

Annabel McFarlane

JLL Head of Strategic Research – Australia.

+61 403 052 672

Email

12394

10251

Annabel McFarlane

Peter Blade

National Head of JLL Logistics & Industrial

+61 417 675 641

Email

12394

9483

Peter Blade