Manufacturing takes the lead as industrial demand rebounds - JLL

Contact

Mar 11, 2025

Manufacturing takes the lead as industrial demand rebounds - JLL

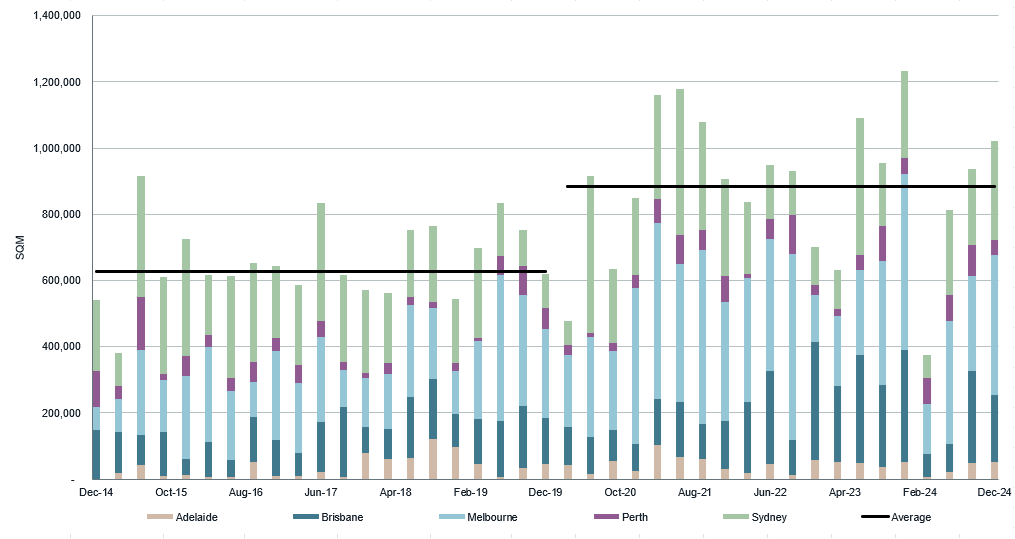

JLL has released its latest industrial research figures for Q4 2024. Businesses in the manufacturing sector led take up volumes in the last quarter of 2024 totalling 343,460 sqm compared to 245,000 sqm for transport, postal and warehousing operators and 141,200 sqm for retailers.

-

JLL Head of Strategic Research – Australia, Annabel McFarlane and JLL Head of Logistics and Industrial – Australia, Peter Blade

JLL Head of Strategic Research – Australia, Annabel McFarlane and JLL Head of Logistics and Industrial – Australia, Peter Blade

JLL has released its latest industrial research figures for Q4 2024. Businesses in the manufacturing sector led take up volumes in the last quarter of 2024 totalling 343,460 sqm compared to 245,000 sqm for transport, postal and warehousing operators and 141,200 sqm for retailers. Over 2024 total manufacturing take up totalled 844,280 sqm, 23% higher than the 10-year annual average.

Elevated supply kept rental growth subdued in most markets. However, national supply weighted average net effective rental growth returned to positive in 4Q24 increasing by 0.28% quarter-on-quarter and 2.39% year-on-year as incentives stabilised in most markets and face rents edged up in some precincts.

The supply cycle is slowing. The number of completions nationally declined for a second consecutive quarter to 649,570 sqm, with a healthy level of precommitment of 63%. However, 2024 set a new 30-year record for industrial completions at 3.1 million sqm.

Key Findings:

- East Coast states accounted for 86% of all occupier demand in 2024.

- Melbourne: 1.24 million sqm

- Sydney: 854,000 sqm

- Brisbane: 632,800 sqm

- Every market except for Perth recorded higher gross take up than their respective 10 year quarterly average in 4Q24.

- Melbourne had the highest volume of take up and remains the market with the lowest vacancy despite an uptick to 3.31% in 4Q24. Vacancy increased in Sydney to 4.16% and in Brisbane to 3.94% over the quarter

- However, sublease vacancy declined across tracked markets: Sublease vacancy declined by over 56,000 sqm to 491,500 sqm in 4Q24 and totals 0.75% of all available space.

JLL Head of Strategic Research – Australia, Annabel McFarlane, said, “The numbers tell us that the demand side of the equation is resilient despite weak consumer and business confidence indicators. The RBA’s decision to reduce the cash rate target by 25 basis points at this month’s meeting will further bolster industrial and logistic demand. Reducing sublease space is also an encouraging sign that businesses have confidence in forward orders and contracts over the near term.

“Construction starts slowed significantly in the second half of 2024 which means a declining supply cycle through to mid-2025. That bodes well for face rental growth and stabilising incentives through 2025.”

JLL Head of Logistics and Industrial – Australia, Peter Blade, said, "Developers are looking to lock in pre-commitments before commencing construction on projects. Our research shows that under construction stock has decreased 17% whilst pre-comm levels have increased by 6% quarter-on-quarter. Occupiers are focused on operating efficiency and getting the size, building quality and location of leased spaces right, both from a sustainability point of view but more importantly a cost perspective.

“Landlords and owners need to be cognisant of local market conditions. We are advising our clients on competitive environments which can vary enormously between and within precincts depending on building size and quality."

National Logistics and industrial gross take up by quarter

Important Information:

Contact details:

Annabel McFarlane

JLL Head of Strategic Research – Australia.

+61 403 052 672

Email

12620

10251

Annabel McFarlane

Peter Blade

National Head of JLL Logistics & Industrial

+61 417 675 641

Email

12620

9483

Peter Blade