JLL APPD Market Report - Sydney

Contact

Jul 12, 2023

JLL APPD Market Report - Sydney

According to, Annabel McFarlane, Senior Director - Research, Australia, record stock delivery and rental growth were evident in 2022 amid considerable yield softening.

JLL have released their APPD market report. Annabel McFarlane, Senior Director - Research, Australia, said record stock delivery and rental growth were evident in 2022 amid considerable yield softening.

Subdued take-up continues amid low availability

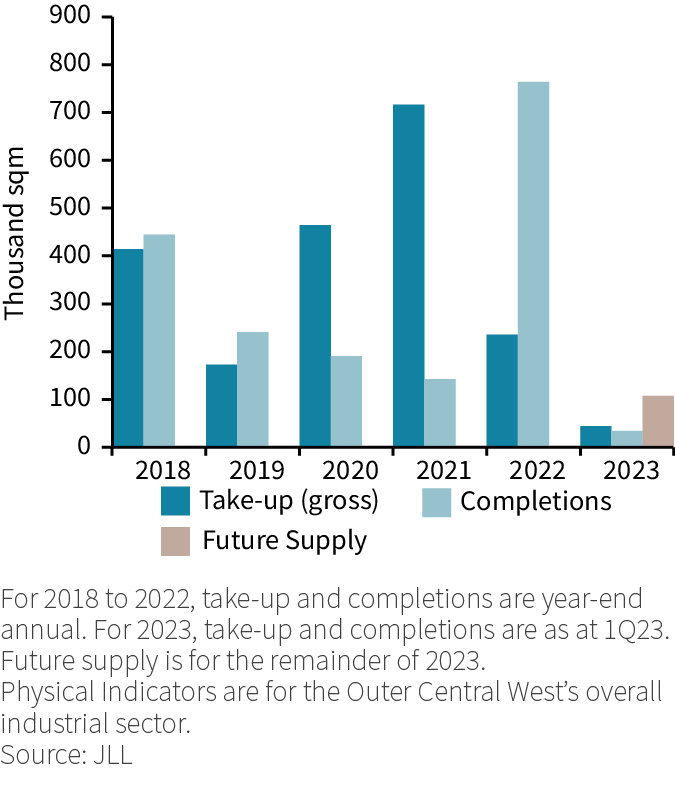

- Gross take-up in the Sydney industrial market was below average for the fourth consecutive quarter in 1Q23, totalling 110,150 sqm. Total take-up reduced by 5% relative to 4Q22 and was 51% below the 10-year quarterly average (225,520 sqm).

- Demand was led by the Transport, Postal & Warehousing sector accounting for 35% of gross take-up (38,150 sqm). The Manufacturing and Construction sectors were responsible for the majority of remaining take-up, accounting for 19% (21,330 sqm) and 13% (14,720 sqm), respectively.

New supply continues to be impacted by construction delays

- Three projects reached practical completion in 1Q23, totalling 68,970 sqm of new stock, a level 49% below the 10-year quarterly average (135,970 sqm). Despite supply chain disruptions easing, new stock delivery continues to be restricted by high construction costs and increasingly limited land availability.

- JLL is currently tracking about 617,200 sqm of stock under construction in the Sydney industrial market, 38% of which has been pre-committed to. Over the next six months, 299,900 sqm of new stock is due to come to market, 38% of which is currently pre-committed. New stock delivery over the next six months will be heavily weighted towards the Outer South West precinct (64%).

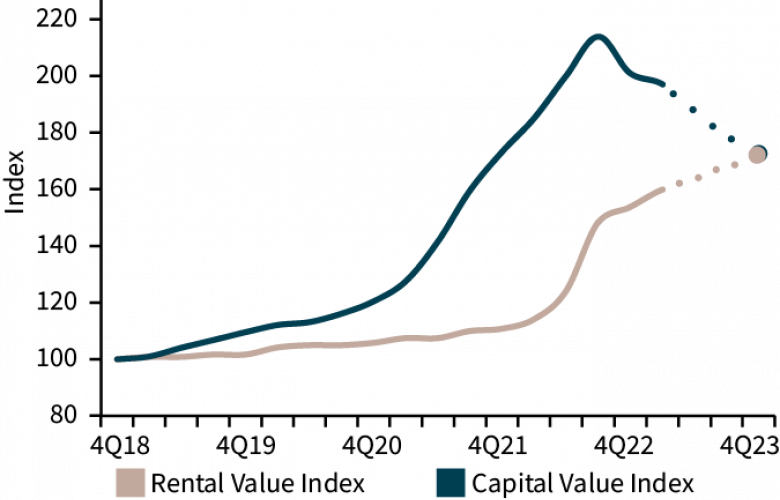

Strong rental growth remains, following record year

- Subdued speculative stock delivery and increasingly tight availability continue to place upward pressure on rental rates. Prime rental rates grew across all precincts in 1Q23, with the Inner West experiencing the most significant growth at 8.7% q-o-q. Secondary rents outpaced the prime market in 1Q23, with the Outer South West experiencing the highest growth at 10.5% q-o-q.

- Transaction volumes increased by 9% in 1Q23, totalling AUD 850.8 million, 67% above the 10-year quarterly average (AUD 510.7 million). New development sites accounted for 44% of transaction volumes, while investment sales comprised 32%. One owner-occupier acquisition accounted for the remaining 25%.

Outlook: Further rental growth and yield softening to remain

- Despite subdued gross take-up, demand for space from occupiers remains strong. However, this is ultimately restricted due to continued low vacancy and limited speculative stock delivery. Easing supply chain delays, tempering construction costs, and existing structural tailwinds are likely to support confidence and strong new stock delivery in the Sydney industrial market.

- Rental growth is expected to remain strong over the remainder of the year before stabilising in 2024. Further yield softening is expected amid continued rental growth in a high bond rate environment.

Important Information:

Contact details:

Contact details:

Annabel McFarlane

JLL Head of Strategic Research – Australia.

+61403052672

Email

11487

9471

Annabel McFarlane